This month approximately 130 million people will begin receiving tax rebates totaling over $100 billion from the IRS as part of the economic stimulus package that was signed into law this February. The rebates will continue to be received throughout the spring and summer.

While most of these funds will be used for other purposes, some of the tax rebates will reportedly be donated to charity. According to the Association of Fundraising Professionals’ report on a recent Associated Press poll, some 4% of the people surveyed intend to use their tax rebate to support a charitable cause. A separate CNN/Opinion Research Corporation poll found that 3% said they will donate the extra money to charity.

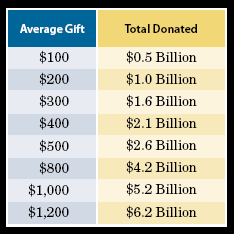

This could translate into millions of contributions and several billions of dollars worth of extra gifts this year. Using the 4% figure, if 5.2 million rebate recipients gave all or a portion to charity, the following gifts would result:

These gifts might even help offset downward pressure on giving that sometimes accompanies a recession or economic downturn.

The additional rebate-associated giving is the latest example of how tax policy can impact philanthropy. In 2005, the removal of AGI limitations for charitable gifts included in the Katrina Emergency Tax Relief Act spurred an additional $11 billion in charitable giving. Then, the 2006 Pension Protection Act included a provision for persons over 70½ to make direct transfers from IRAs to charity. Over $135 million in such transfers have been reported to the National Committee on Planned Giving thus far, and it’s possible that additional unreported IRA transfers could push the total into the $500 million to $1 billion range. Note gifts from 4% of rebate recipients of just $300 on average would result in more gifts than the IRA provisions.

Who will benefit?

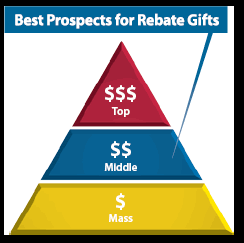

While every charity is a potential recipient of tax rebate gifts, those who communicate the concept to potential contributors are likely to be the biggest beneficiaries. Who are the best prospects for tax rebate gifts? The answer may surprise you.

Instead of your wealthiest donors, or the mass of lower-dollar donors, the best prospects will likely be found among your mid-level donors. Most of the top-level donors will be ineligible for tax rebates because of income limits which phase out the benefit for singles with incomes over $75,000 or couples who earn over $150,000. Many lower-dollar donors may use this tax rebate windfall to pay debts or to purchase necessary goods or services. Some of these donors will give all or part of the tax rebate to charity, but most will not.

Remember, people tend to give from discretionary income and assets. Thus, the best prospects may be found among those people in the middle of your donor base for whom the rebate represents increased discretionary income and who do not need the funds to pay bills, go out to dinner, or to buy more “stuff.” We believe that the comfortable, middle-class, better-than-average donor will be the best prospect for these gifts.

They will be most likely to appreciate additional funds from which to make charitable gifts, with the knowledge that funds given to charity will be expended on salaries and programs, thereby providing a direct economic impact.

Those in the middle group are in the best position to consider additional charitable gifts this year. Many could make gifts in the $100 to $1,000 range using funds from their rebate. In some cases, those who immediately save the money may, when prompted, reconsider and decide to give all or a portion of their rebate. Almost every charitable organization has hundreds, or even thousands, of donors who fall into this mid-range. We anticipate that the vast majority of these extra rebate gifts will come from donors who have in the past made gifts of between $100 and $5,000.

Tax incentives for rebate gifts?

When you communicate with those donors in the mid-range group about the charitable gift potential of the tax rebate, be sure to explain the potential double benefit they can expect from such gifts.

Example: If Sue decides to save her $1,000 rebate, she might earn 2% if she puts that money into her savings account. However, if Sue decides to make a charitable gift of $1,000 of her tax rebate, she will enjoy up to a 25% return on her money. How? Sue does not have to report the rebate as taxable income, but she will be allowed to deduct $1,000 for her charitable gift on her 2008 tax return. In her 25% tax bracket, this results in a $250 tax savings. She thus enjoys $1,250 in benefit from her rebate—$1,000 donated to charity plus the $250 she enjoys in tax savings as a result of her gifts. State income tax savings may further increase her benefit.

Reaching the right group

To receive maximum benefit from these gifts, charities should plan now to communicate the opportunity to prospects this spring and summer. Ideally, use a multi-layered marketing effort that provides overlapping messages via the appropriate mixture of special targeted mailings, inserts in existing appeals, ads and articles, postcards, e-mail, and web content. (See www.sharpenet.com/taxrebatesandgiving or page 7 for more information.)

There is likely to be significant competition for these funds, so it is essential for nonprofits to get this message out often and repeatedly in order to secure a maximum slice of the tax rebate pie.