With the last several years of unexpected government funding cuts and a global pandemic, it has become increasingly clear that nonprofits must have planned giving as part of their fundraising strategy.

With the last several years of unexpected government funding cuts and a global pandemic, it has become increasingly clear that nonprofits must have planned giving as part of their fundraising strategy.

Surprisingly, there are many reasons leadership doesn’t support adding a dedicated planned giving component to their fundraising efforts, some of which are based on misconceptions, myths and fear.

Myth #1: Planned giving hurts annual giving.

The Reality:

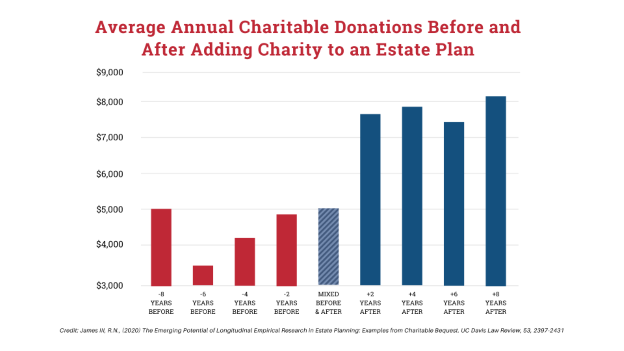

Some believe that if you ask a donor to include you in their estate plans, they will stop making current gifts. Well-known fundraising researcher Dr. Russell James has gathered data that proves this is not true. In fact, his research shows that donors who have added charities to their estate plan give 77% more in annual gifts than those who have not included a charity in their will. Additionally, while fundraisers typically see a decline in annual gifts as donors pass the age of 65, the donors in this study were 73 and older, making the increase in annual support even more significant (see chart below).

Myth #2: All planned gifts are deferred gifts.

The Reality:

This argument is based on a misunderstanding of what a planned gift is. Sharpe Group founder—Robert F. Sharpe Sr.—defined the term in the August 1972 issue of Give & Take (now Sharpe Insights):

To make a deferred gift, a person decides to give at some future date, either a number of years from now or at death. A deferred gift is a present decision to make a future gift, evidenced by a legal contract.

While the name, deferred giving, is best known to professionals in the field, it is not a term that communicates very much to the donor. Therefore, we suggest the term ‘planned giving.’ When a person makes a planned gift, it suggests forethought.

Following in his father’s footsteps, former Sharpe Group president Robert F. Sharpe Jr. added additional details to this definition in the March 1988 issue of Give & Take:

A planned gift is any thoughtful gift of any amount, given for any purpose—operations, capital expansion, or endowment—whether current or deferred, which requires the assistance of a knowledgeable staff person, a qualified volunteer, or the donor’s advisors to complete. In addition, it includes any gifts of such magnitude as to be carefully considered in light of estate and financial plans.

“Planned” does not refer to the future here; rather, it refers to the planning process. This is why some organizations have begun to adopt the term “gift planning,” which Sharpe suggested in the October 1999 edition of Give & Take.

Examples of current planned gifts include QCDs, noncash gifts, gifts from DAFs and charitable gift annuities.

Myth #3: Planned giving is only for older, wealthier donors.

The Reality:

Depending on the planned gift, often older, but not necessarily wealthier.

There is a reason that people associate planned giving with a more mature crowd: As people age, they begin thinking more seriously about estate planning and their legacy because they have family to consider and their assets have grown. At that point in their lifecycle, they are more likely to have the capability and the motivation.

However, age is not a factor when it comes to donating appreciated securities, and your younger donors may have the capacity to make these types of gifts when they realize the tax savings available.

Segmenting your donor lists by age and wealth and targeting messages based on these demographics can help you uncover your best planned giving prospects.

Stay tuned to the Sharpe blog as we cover more myths and the best ways to counteract them in future posts.

Teri Sullivan is vice president of marketing for Sharpe Group and serves as co-producer of the podcast Sharpe Insights: Conversations With Your Planned Giving Experts. You can connect with Teri via email or on LinkedIn.

Teri Sullivan is vice president of marketing for Sharpe Group and serves as co-producer of the podcast Sharpe Insights: Conversations With Your Planned Giving Experts. You can connect with Teri via email or on LinkedIn.