It’s well known in certain quarters that a charitable lead annuity trust (CLAT) works well in a low-interest-rate environment.

It’s well known in certain quarters that a charitable lead annuity trust (CLAT) works well in a low-interest-rate environment.

We’re in such an environment, so let’s drill down into the CLAT.

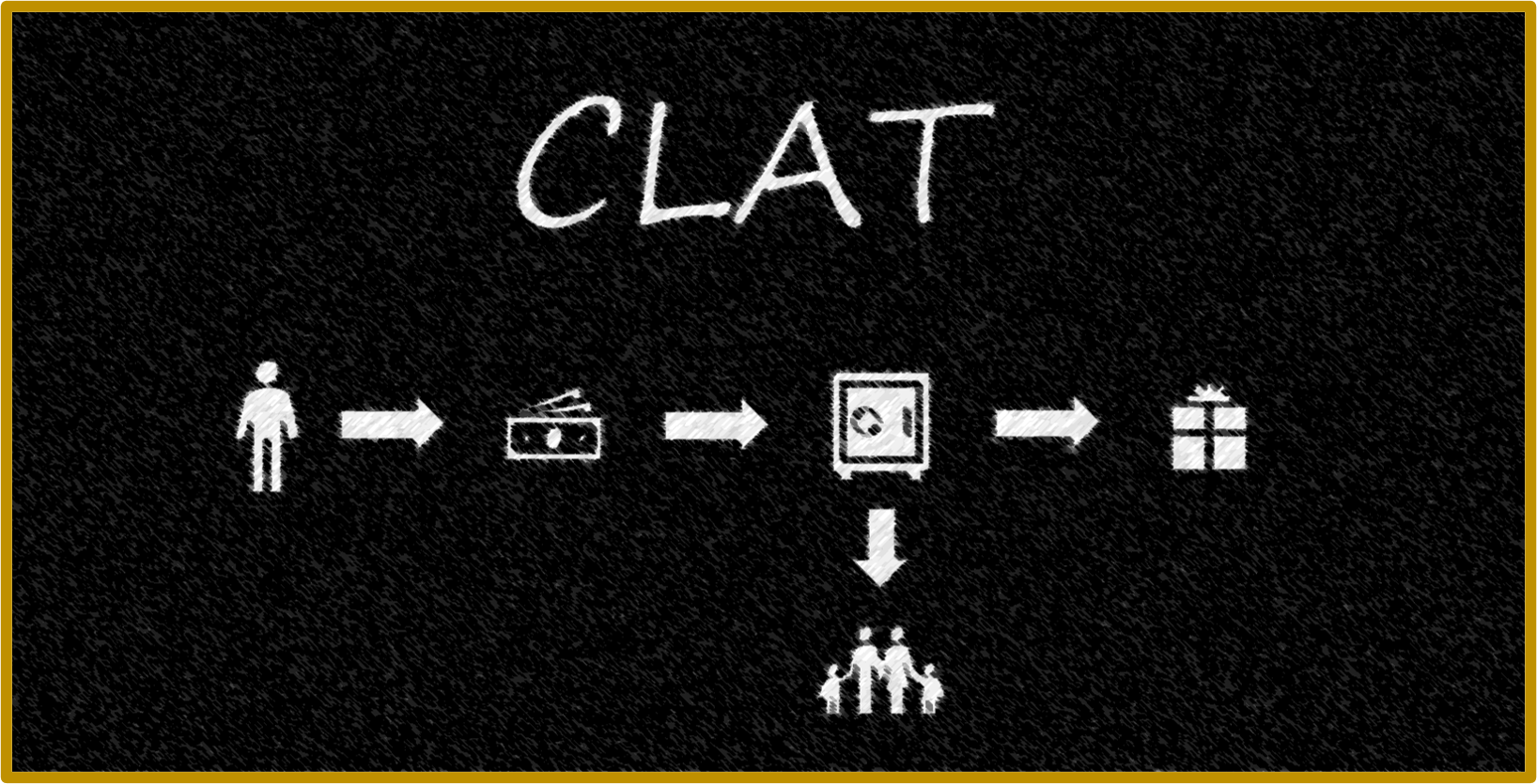

First, the big picture. A CLAT makes an annuity payment to charity for either a fixed term of years or a life. The life may be that of the trust’s creator. It also may be that of certain of the creator’s family members, although I’ve never worked on such a CLAT.

- At the end of the trust term, all trust assets pass to noncharitable parties, typically the donor’s kids.

- The kids generally receive the assets free of income tax.

- Any growth in the value of CLAT assets also passes to the kids free of estate tax.

OK, so you know all that. So let’s up the ante and look at a CLAT that’s used by a few sophisticated estate planners for very wealthy clients. Here’s how it works. Donor sets up a grantor CLAT (meaning all CLAT taxable income will be taxed to Donor). The CLAT is designed to run for Donor’s life and to have an escalating payout to charity. Details omitted, the yearly payout is small but non-negligible until Donor dies. Upon Donor’s death, the CLAT makes a sizable balloon payment to charity and then terminates.

Donor funds the CLAT with a fully paid insurance policy on Donor’s life. And maybe with some liquid assets. The insurance policy [1] doesnt throw off any taxable income (so it doesn’t produce a grantor trust problem) and [2] provides the means for the balloon payment.

Bottom line: Donor gets an up-front income tax charitable deduction for the initial present value of the charitable payout. Donor is able to use the CLAT to pass the “excess” insurance proceeds to Donor’s kids free of estate tax.

This type of CLAT, in my experience, is wielded by high-end financial planners who know the ins and outs of life insurance.

If you have questions about CLATs, send them to info@SHARPEnet.com. I’ll answer them next time.

Giving Through Charitable Lead Trusts

In our current economic environment, charitable lead trusts are appealing for certain donors who want to make a significant gift over time while having property ultimately returned to them or their heirs. Sharpe Group’s Giving Through Charitable Lead Trusts booklet highlights what this versatile gift planning tool can accomplish for your donors. Use this publication as an inclusion in a letter to select high-level donors, as support materials to accompany gift proposals or in a mailing to local financial advisors. Imprinted booklets allow you to add your organization’s logo and contact information to the front and/or back cover. Unimprinted booklets may be used by multiple fundraisers or departments and may be personalized via a stamp, sticker or business card. For more information about ordering Giving Through Charitable Lead Trusts, click here.

In our current economic environment, charitable lead trusts are appealing for certain donors who want to make a significant gift over time while having property ultimately returned to them or their heirs. Sharpe Group’s Giving Through Charitable Lead Trusts booklet highlights what this versatile gift planning tool can accomplish for your donors. Use this publication as an inclusion in a letter to select high-level donors, as support materials to accompany gift proposals or in a mailing to local financial advisors. Imprinted booklets allow you to add your organization’s logo and contact information to the front and/or back cover. Unimprinted booklets may be used by multiple fundraisers or departments and may be personalized via a stamp, sticker or business card. For more information about ordering Giving Through Charitable Lead Trusts, click here.

Sharpe Group will continue to post helpful information for you here on our blog and on our social media sites. If this blog was shared with you and you wish to sign up, you can do so at www.SHARPEnet.com/blog.

We can be found on Facebook, Twitter and LinkedIn @sharpegroup.

We welcome questions you’d like us to address. Email us at info@SHARPEnet.com and we’ll share your question and our thoughts in this blog and on social media.