Are you following the Sharpe Group blog? We regularly post information in our blog that is helpful for gift planning, including up-to-date information affecting your organization. Sign up here to follow our blog.

Are you following the Sharpe Group blog? We regularly post information in our blog that is helpful for gift planning, including up-to-date information affecting your organization. Sign up here to follow our blog.

The following article is a blog post by Jon Tidd that first appeared on December 28, 2015 and was a follow-up to an earlier blog post, “When Is a Gift Complete for Tax Purposes?”

The prescription is simple in principle, but sometimes not so simple in practice: Stick to the facts. That’s it. It applies to all gift situations, and no one (especially a strong-willed donor) can argue rationally against it. Let’s look at some gift situations and see how to apply this prescription.

SITUATION 1: On January 4, a Monday, an organization receives a $500 check dated December 31, a Thursday. The envelope is postmarked January 2, a Saturday.

The tax law provides a gift made by a check deposited in the mail is complete on the date of mailing, not the postmark date, provided the check clears in due course. What is the date of mailing here? It’s impossible to tell from the facts. The check could have been deposited in the mail on December 31 (after hours), January 1 or January 2.

Not to worry; simply state the basic facts on the gift receipt. What are the basic facts? They are: [1] check was received via USPS on January 4; [2] check amount is $500; [3] check is dated December 31.

Those are the facts. (Also state, by the way, whether the donor received any goods or services in consideration of her gift.) Leave it to the donor to claim when the gift was made on her tax return. If the donor insists the gift was made in December, it’s acceptable to write on the gift receipt, “…which you have stated you mailed in December…”

SITUATION 2: An organization receives in its account on January 4, a Monday, 1,000 shares of MMM stock. The organization is able to verify the stock was wired out of the donor’s account on December 31.

We don’t know the date of gift for tax purposes; the law is unclear. But we know these facts: [1] 1,000 shares of MMM were received on January 4; [2] the shares were wired out of the donor’s account on December 31. Although the gift receipt here need not state a value for the stock, the mean values of a MMM share on 12/31 and 1/4 are facts. It’s OK, but unnecessary, to state those values on the gift receipt.

Time for a review

Gift receipting is important. As in the case of other organizational policies, it is advisable to periodically review your gift acknowledgement forms and practices.

Gift receipting is important. As in the case of other organizational policies, it is advisable to periodically review your gift acknowledgement forms and practices.

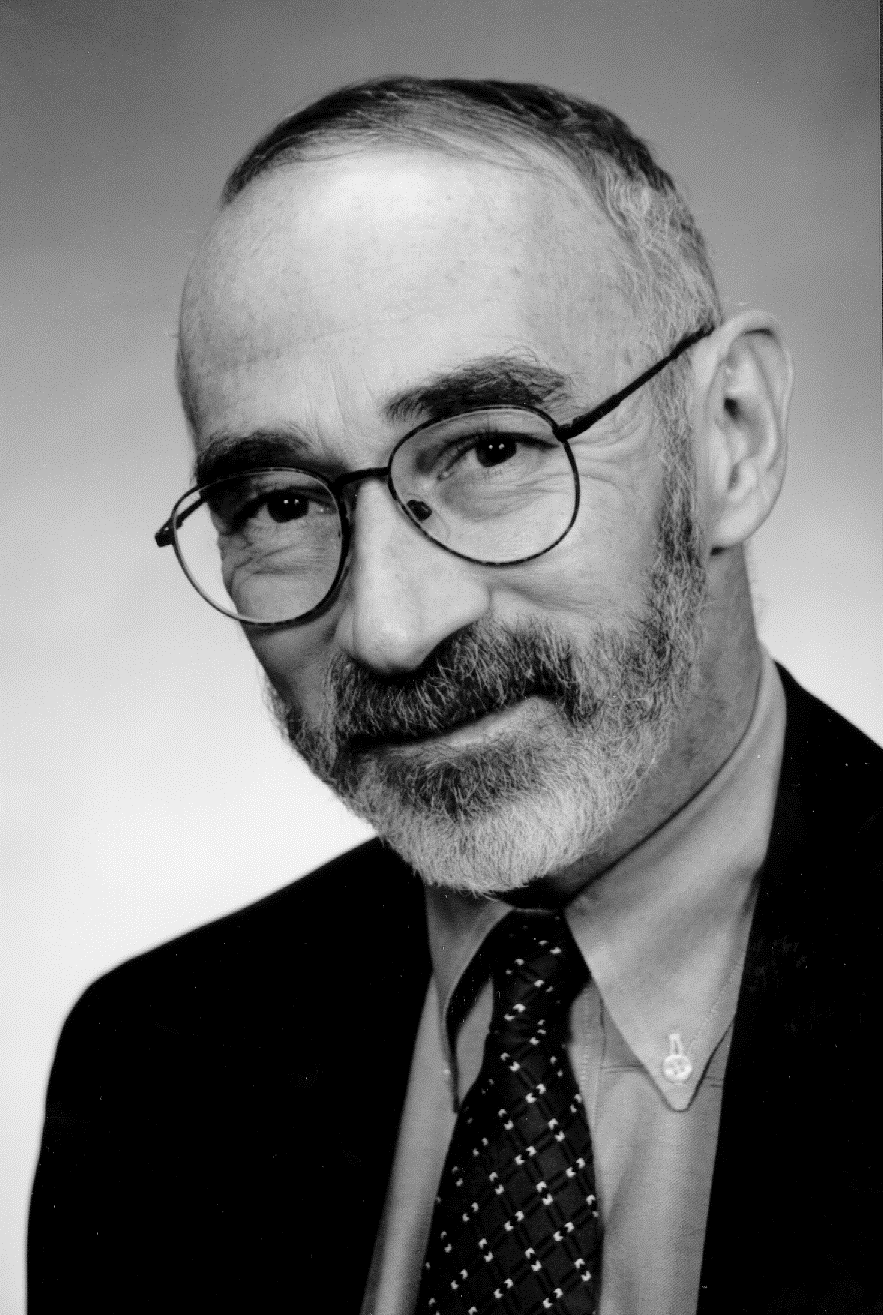

Jonathan Tidd has served as a technical resource to Sharpe Group for over 30 years. Jon is an attorney whose practice is limited to advising charitable organizations on gift planning issues. He is a member of the Arizona, Connecticut, Illinois (inactive), Indiana (inactive) and New York Bars. His clients include a wide range of educational, health care, arts, human rights and social service organizations. His articles on charitable gift planning have appeared in The Journal of Taxation; Estate Planning; Taxes—The Tax Magazine; Trusts & Estates and other professional journals.