At the 25th Conference on Gift Annuities held this spring in Seattle, Washington, the American Council on Gift Annuities announced its recommendation for rates to take effect July 1, 2002.

While there were changes to the various assumptions underlying charitable gift annuity rates, the recommended rates remain basically unchanged.

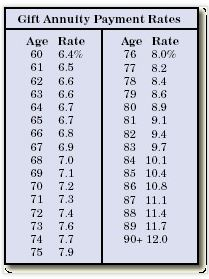

The ACGA board voted not to change the recommended payment rates for immediate gift annuities except for single-life annuitants younger than 39 and two-life annuitants younger than 57. As the majority of gift annuitants each year are age 70 and beyond, these changes should have little or no impact on most organizations and institutions that issue charitable gift annuities.

This year’s recommendations are based upon extensive review and analysis that included expert assistance from actuaries and representatives of financial institutions. Their findings resulted in changes in both assumed mortality rates and expense assumptions.

It has long been assumed that planned giving donors live longer than the general population. For this reason, female life expectancies (used to calculate rates for all gift annuitants) in the past have been set back one year from the life expectancy of the average American woman. As part of this year’s review, the ACGA authorized a mortality study to examine data from 26 organizations, covering approximately 25,000 gift annuities over a five-year span ending December 31, 2000. Based upon this analysis the age setback determined by the female life expectancies under the Annuity 2000 Table was increased by six months.

In addition, annual assumed expenses for investment and administration were increased .75% to 1.0%. The assumed total annual return on investments was also increased .25% to 6.75%.

Practically speaking, the increases in the expense factors and life expectancies were offset by the increase in the assumed total investment return on gift annuity reserves. The net effect is that there is no change in the recommended rates for most annuitants.

For more information

Additional information about charitable gift annuities and the recommended rates may be obtained from:

American Council on Gift Annuities

Gloria Kermeen, ACGA Administrator

233 McCrea Street, Suite 400

Indianapolis, IN 46225

Voice: (317) 269-6271

Fax: (317) 269-6276

acga@acga-web.org

Notes:

1. The gift annuity rates above are for ages at the nearest birthday.

2. These annuity rates, for both immediate and deferred annuities and for both single life and two lives, should not be used if the gift portion, based on IRS tables and the applicable discount rate, is not more than 10% of the amount paid for the annuity. The current recommended rates will result in a charitable deduction of at least 10% if the IRS discount rate (CMFR) is 5% or higher. If the CMFR falls below 5%, rates at certain young ages may have to be reduced to meet the 10% deduction requirement. Popular gift calculation software will typically include automatic warnings should an adjustment be required to meet the 10% minimum requirement.