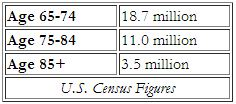

Over the past few years much has been written about the aging of America and how a larger pool of older Americans will create, among other things, a golden age of philanthropy through unprecedented amounts of assets passed via estates. Consider the fact that the portion of the American population over the age of 65 increased eleven-fold from 1900 to 1994, as compared with just a three-fold increase in the population under that age during the same period. By the mid-1990s, older Americans represented one-eighth of the U.S. population and can be categorized as follows:

Health care advances and lifestyle choices have shifted the more dramatic increases in the number of older Americans to the group comprising the oldest of the old — the over-85 age group. In a few more years the baby boom generation will begin contributing to the number of newly minted 65-year-olds. In the meantime, indications are that elderly population growth rates will be more modest during the 2001-2010 period. This is a result of decreased birth rates during the Depression years and World War II.

Of special interest to gift planners

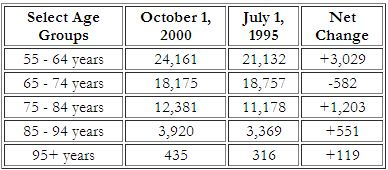

Based upon recently released population estimates from the U.S. Census Bureau, there has, as would be expected, been a decline in the number of persons age 65 to 74 — an age range of special interest to gift planners.

The dip in 65- to 74-year-olds is a direct result of the decline in birth rates in the 1930s. The decrease in a portion of the prospect group for planned gifts may have already begun to affect those planned gift development programs without plans in place designed to adapt to this phenomenon.

Dealing with the dip

Many successful programs have already begun to implement age and wealth-based planned gift strategies to deal with potential problems caused by the decreased numbers of persons aged 65 to 74. Examples include efforts to increase market share among the nearly 20 million persons in this age range. Other programs have begun marketing planned gifts to the larger constituency in the next youngest age group. This solution must be carefully considered to avoid attracting gifts from persons who are at an age where such gifts may not be optimal. For younger donors, consider a shift to term of years trusts to meet specific objectives, or plans to provide for elderly relatives and others. Gift plans that “return ” the donor’s funds over time, such as grantor lead trusts or relatively high payout CRTs, may also be appealing to members of the emerging group of 55- to 65-year-olds.

Traditional gift planning techniques will continue to be attractive to the 75- to 84-year-old group. Fixed income alternatives like gift annuities and annuity trusts could, in fact, become even more popular in a period of low inflation and low interest rates (See page 1 for more on this topic). Communication approaches may need to be adapted for these very different audiences. What is appropriate for a 75-year-old may miss the mark for a 55-year-old and vice versa.

Special approaches may also be particularly useful with the over-85 age group, recognizing the social, economic, health, and demographic concerns of the oldest of the old. As this group grows and is active to an older age, programs that continue to serve donors in this oldest age group can be expected to be of increased importance. Gift annuities and bequests from this group may make the difference in programs where smaller numbers of those in the 65- to 75-year-old group can be expected to result in fewer gifts. Programs that recognize the changes that demographic shifts portend will continue to be successful, especially those that recognize that a one-size-fits-all approach may be less productive when spanning age groups from age 55 to age 90 or older.