Most fundraisers know how important the critical year-end giving season can be to their fund development efforts. The calendar year-end provides a natural deadline for tax and other purposes that leads many to routinely assess their financial condition. As a result, the number of regular and special gifts tends to increase during the final three to four months of the year.

In the busy year-end season, gift planners are more likely than ever to encounter gifts that may raise difficult questions. This “Planning Matters” column will address some of the issues that may arise concerning various gifts between now and December 31. Taking time now to consider these topics may help to make your gift development efforts more successful.

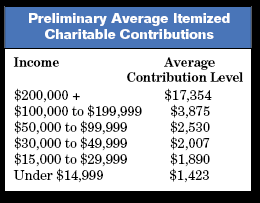

Question: Who gives to charity in the United States? How much do they give?

Answer: See the article on page 1 for the latest Giving USA estimates, which have just been released. It has been estimated that over 90% of adults make gifts to charity each year and over 34% of individual taxpayers itemize their deductions for income tax purposes. Based on the 2005 U.S. Master Tax Guide, published by Commerce Clearing House (CCH), those donors give the following amounts to charity on average, based on their income level.

Question: What form do their gifts take?

Answer: While most gifts are made with cash, usually in the form of a check, a smaller number of larger gifts can be expected to come in the form of non-cash assets. From the charity’s perspective, highly marketable assets such as publicly traded securities are preferred. Gifts of many types of other intangible personal property and real property may also be de-ducted at their full fair market value.

Question: How is the value of these gifts determined?

Answer: For non-cash gifts other than publicly traded securities that are valued at less than $5,000 (or $10,000 for closely held securities), the donor is responsible for substantiating the value of the gift on IRS form 8283. For larger gifts, qualified appraisals may be required. To learn more about form 8283, visit the IRS’s Web site at www.irs.gov and create a search for 8283. You may also wish to review IRS publication 526 on charitable contributions and IRS publication 561 on determining the value of donated property.

Question: Do limits on itemized deductions for high-income taxpayers affect charitable gifts?

Answer: Taxpayers filing jointly must reduce their total itemized deductions by 3% of the amount by which their adjusted gross income exceeds $142,700. In most instances, a donor’s charitable gift will not be affected. The reduction occurs whether or not charitable gifts are made, and other fixed deductions such as mortgage interest and taxes serve to “absorb” the reduction, arguably leaving the charitable deduction intact.

Question: What about donors who are or may be subject to the alternative minimum tax?

Answer: While the benefits of many deductions and adjustments are lost for alternative tax purposes, donors and development officers alike will be glad to know that charitable gifts may be deducted for both regular and alternative minimum tax purposes.

Question: What should I know about gifts of tangible personal property?

Answer: Usually such property has depreciated and the donor will be able to claim the current resale value, not the original purchase price. However, in the case of appreciated assets such as art, antiques, or other collectibles, the donor may be entitled to claim a deduction for the full fair market value if it can be anticipated that the item will be part of a related use, i.e., a gift of a painting to an art museum versus the gift of the painting to be auctioned for charitable purposes. As the capital gains tax on tangible personal property is 28% (as opposed to 15% for most other capital assets), many donors may be best served by donating tangible personal property rather than other assets, as the capital gains tax savings may be greater.

Remember to review your gift acceptance policies and procedures early and make sure that others do so as well. In particular, review the sections dealing with gifts of publicly traded securities and real estate. It may also be beneficial to review lists of past donors of non-cash property and other contributors of large amounts before the year-end season begins to single them out for special communications. In addition, consider taking the time to develop individualized strategies for the handful of top donors and mass strategies for larger groups. See page 7 for information on brochures that may be helpful in communicating with donors to encourage substantial year-end gifts.