With the ups and downs that the stock market has experienced so far this year, one might expect some investors to be reconsidering their level of commitment to a market experiencing this kind of volatility. But news reports indicate that the roller coaster market has thus far not yet shaken the confidence level of most investors. It appears that both seasoned and novice investors recognize that markets will invariably fluctuate. In addition, many investors realize that short-term downward swings may even provide opportunities to buy additional stocks at a discount.

Stocks boost giving

According to the Giving USA reports on charitable giving in America,gifts of appreciated securities have been one of the prime reasons that charitable giving reached record levels in recent years. Recently released Council for Aid to Education reports credit strong stock markets with driving an 11% increase in giving to higher education this year. If the current atmosphere of uncertainty and volatility surrounding equity markets continues, however, what impact might we expect in charitable giving, and what strategies may be beneficial to planned and major gift prospects in the months ahead?

An increase in cash gifts?

Those who decide to reduce their exposure in the stock market this year may well find that they have significant amounts of cash on hand as they take their profits, and in some cases losses, in the market.

Some will reinvest in other securities, but many will place their cash “on the sidelines.” For these persons, 2000 may be an excellent time to use some of their gains from the long bull market to complete outstanding pledges and otherwise make larger than usual cash gifts in 2000. Such gifts can help to offset capital gains taxes that would otherwise be due as a result of taking gains in the market.

There are other ways to combine charitable giving with realignment of investment portfolios.

Three options

We start with the fact that there are really only three possible scenarios for investment markets — they can go up, go down, or trade at current levels. Each of these different scenarios provides planning strategies that can help your donors meet both personal and charitable goals with gifts of appreciated securities.

If a donor believes that the market is headed downward, one strategy would be to make charitable gifts with appreciated securities to conserve cash. This strategy would allow the donor to fulfill charitable obligations with “paper profits ” that the donor thinks may be further eroded by future decreases in the market while, at the same time, preserving cash for other purposes. The donor enjoys a federal, and perhaps state, income tax deduction based on the full value of the donated assets, and capital gains tax is bypassed entirely.

If your donor is uncertain as to which direction the market may go,you might want to suggest that, instead of giving cash, he or she consider making outright gifts using appreciated securities. Then the donor can use the cash that might otherwise have been donated to repurchase additional shares of the same stock at today’s value. That way, if investments lose value in a market correction, the donor will have a capital loss to declare for tax purposes. On the other hand, if the markets go up, the donor will enjoy a new, higher cost basis in the stock that “replaced ” the donated stock. This strategy, sometimes referred to as “reloading,” may have particular appeal to donors who are receiving large cash bonuses and thus have the funds to give while “replacing ” their investments.

“Balancing” interests

If your donor simply wants to reduce his or her position in the market, the donor may want to consider a combination of giving some shares of stock and selling the remaining shares. This is called a “balanced sale ” of the stock.

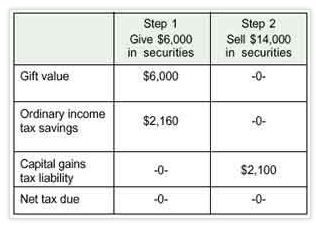

Let’s examine how a balanced sale works. Suppose Bill Turner owns stock worth $20,000. He bought the stock for just $5,000 several years ago. He believes that the stock is unlikely to increase in value in future years and he would like to sell it. He does not, however, wish to pay capital gains tax of as much as $3,000, which would leave him with net proceeds of no more than $17,000.

Mr. Turner is also interested in making a charitable gift of approximately $6,000 while enjoying the greatest tax savings in his 36% tax bracket.

Here is how a balanced sale would help him accomplish both of his goals.

Take a look at the chart above. Note that the $2,160 in tax savings from the gifts more than offsets the $2,100 in capital gains tax due on the securities sold. The tax liability on the portion of the securities that are sold is thus “balanced ” by the tax benefit for the charitable gift portion.

Mr. Turner is able to enjoy cash proceeds of $14,000 and the satisfaction of making a $6,000 gift, a total of $20,000 in value to him, while effectively bypassing capital gains tax liability. Had he sold all of the securities, he would have netted just $17,000 after paying some $3,000 in taxes. Mr. Turner has thus been able to make a $6,000 gift at an after-tax “cost ” of just $3,000.

Giving gains for income

In today’s environment, many donors may wish to use stock that has increased in value in recent years to fund gifts that provide additional income for themselves and/or loved ones for life or other period of time. Funding such gifts can be an excellent way to unlock value from appreciated securities while reducing tax liabilities and providing an additional source of income for future use.

Helping donors

While these strategies may seem obvious to charitable gift planners, it is doubtful that many of your donors have seriously considered the possibility of combining their personal and philanthropic planning. Charitable organizations and institutions must be prepared to assist donors and their advisors with advice about the most effective ways to give securities in today’s economic climate if they hope to reap future rewards.

For more about ways you can communicate the benefits of stock gifts to your donors, check out the Sharpe booklet “A Guide to Year-End Giving.” Explanations of the strategies described above along with detailed examples your donors can understand are featured. See page 6 of this issue for more details.