There is an old fund-raising adage about raising money. As the story goes, a young fundraiser asked an old pro if he could share some “tricks of the trade.” The old-timer thought about the question for a minute and responded, “Find out what somebody has a lot of and ask them for some of it.”

What the experienced fundraiser was getting at was that cash is only one thing to ask for, and it may be better in some cases for the donor to use non-cash assets to complete a gift. Remember that even the wealthiest donors are unlikely to keep more than a small percentage of their assets in a checking account. Regardless of tax consequences and other considerations, the larger a gift is, the more likely it is to be completed in a form other than cash.

New information from the IRS

The overall importance of non-cash gifts is becoming more apparent now that the Internal Revenue Service has begun releasing periodic studies of these gifts reported by taxpayers as itemized income tax deductions. The first such report, released in 2006, revealed that taxpayers reported more than $37 billion in non-cash gifts for the 2004 tax year.

Over the years, the IRS has been concerned about the overvaluation of non-cash gifts and has instituted a variety of rules and regulations designed to police the valuation and substantiation of such gifts. IRS Forms 8282 and 8283 and their instructions are a result. Publication 1771 addresses the charities’ acknowledgements to the donors for various gifts and Publication 561 provides information on valuing gifts.

More recently the IRS has tightened the rules for gifts of automobiles and other items such as used clothing and furniture, which the IRS and Congress believed had been overvalued in many cases.

Despite the IRS’s apparent interest in gifts of personal property of various types, most fundraisers are not that interested in gifts of a 10-year-old Chrysler Town and Country minivan or determining whether used clothing and household items are in “good condition.” Gifts of securities, real estate, and other valuable property are the prize that experienced fundraisers seek.

The latest data

The IRS has just released its latest report on Individual Non-Cash Contributions covering the year 2005. That year, over 25 million taxpayers who itemized deductions reported over $41 billion in charitable contributions of non-cash property.

While the number of contributors remained roughly the same, the amount of non-cash contributions increased 11% over the $37 billion reported for the previous year. This was a much higher rate of growth than other forms of giving that year.

This double-digit increase occurred in spite of tightened regulations affecting donated vehicles. The number of vehicle donations actually declined by over two thirds, from 900,000 in 2004 to under 300,000 in 2005.

What about the good stuff?

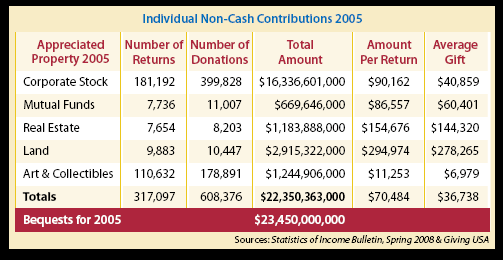

Some charities can use food, clothing, and similar items, but as noted above, most prefer non-cash gifts that can be converted to cash. These would include stocks, bonds, mutual funds, other securities, and real estate. The largest single category of non-cash gifts in 2005 was corporate stock, which totaled $16.3 billion. Real estate or land donations were valued at $2.9 billion. See the following summary:

While the majority of returns claiming non-cash gifts reported clothing, automobiles, and household items, nearly 320,000 returns reported gifts of the “good stuff.” These accounted for over half the non-cash gifts totals at more than $23 billion.

To put this into perspective, that amount was almost the same as the $23.45 billion reported by Giving USA for bequest income in 2005 or the $23.09 billion reported for bequests for last year. For further perspective, the 320,000 people reporting non-cash gifts was approximately 60% more than the estimated 200,000 charitable estates for 2005.

Once again, age matters!

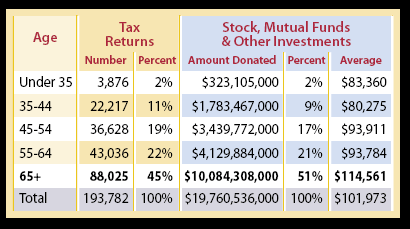

Interestingly, age appeared to be an important factor to consider. Note from the chart below that persons over age 55 gave nearly 72% of stock, mutual funds, and other investments while those over 65 gave over one-half of these gifts.

In terms of size of gifts, those over 65 gave stock and other investment gifts that averaged over $114,000, 22% more than any other age range. The IRS also reported that overall non-cash contributions averaged 3.6% of contributors’ adjusted gross income (AGI). Those over 55 gave at the average or above, with persons over 65 giving nearly twice as high a percentage of their AGI in the form of non-cash gifts.

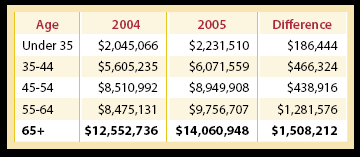

In addition, the over 65 age group showed the largest increase—$1.5 billion—from 2004 to 2005:

Experienced fundraisers know that age does, in fact, matter when marketing gift annuities, bequests, and other planned gifts that mature at the death of one or more individuals. According to the American Council on Gift Annuities, the average age of persons at the time they enter into a gift annuity is 78. Many other studies show that the majority of bequests that leave funds to charity come from wills executed by persons 78 or older as well.

IRS data now supports the fact that each year a disproportionate amount of non-cash gifts are also coming from older individuals. This should be taken into account, especially when working with older, wealthier persons, those found in the C1 quadrant of the Sharpe Gift Planning Matrix.©

Reaching the right donors

Given the fact that “quality” non-cash gifts of securities and other marketable property account for about the same amount each year as bequests, and the primary source for these gifts appears to be older donors, those responsible for fund development efforts might wish to consider whether they are devoting proportionate efforts to encouraging non-cash gifts among seniors in the C1 box as well as wealthy prospects in the A1 and B1 boxes (see the shaded portion of the Sharpe Matrix above.) There is also a smaller group of prospects that may be found in the upper ranges of the A2, B2, and C2 boxes—for example, a 75-year-old donor who funds a gift annuity with highly appreciated, low-yielding stock.

In light of recent fluctuations in the stock market and other factors, this fall might be a good time to consider sending a “mixed message” to your organization’s base of support, especially in cases where age and wealth information are not known for all donors and it is not possible to determine who may be the best prospects among the broader mix of donors for bequests and non-cash gifts. This could be a good time to approach a broader group of donors with information outlining the importance of non-cash gifts along with a message aimed at encouraging legacies in the form of bequests and other planned gifts.

Editor’s note: See page 7 for more information about resources available if you would like to inform your donors this fall about the importance of both bequests and non cash gifts.