One of the items included in the President’s proposed budget has given rise to a great deal of discussion in the press and elsewhere—namely the proposal to raise taxes on the wealthy by taxing a portion of the amount of income they give for charitable use.

Unfortunately, few commentators have correctly interpreted what the actual impact of the proposed changes would be. Some have said that the bill would reduce the amount that the wealthy could deduct from 35% of their gift to 28%. Others have said the savings would be reduced from 35% to 28%. Many of the descriptions are flawed in various ways; some are simply erroneous and/or misleading.

By the time you are reading this article, the issue may have been decided. If the proposed changes have become law, then take a moment to read on to understand what this may mean for fund raising in the future. If the provision has been dropped, then continue reading for a primer on how the charitable deduction actually affects the cost of a charitable gift. If the matter is still in flux, then we hope what follows will be helpful to readers in forming their opinion of the proposal—positive or negative.

Starting at the beginning

Let’s start with the difference between a tax “credit” and a tax “deduction.” Tax credits allow for a relatively straightforward reduction in the amount of tax paid to the government. For example, suppose I earn $100,000 in a given year. If my federal tax rate is 25%, my tax bill would be $25,000. Now imagine there is a tax credit of up to $10,000 for amounts given for charitable purposes. As a “credit,” that amount would be offset against my tax bill and would lower it from $25,000 to $15,000. After taxes, the $10,000 I donated to charity would cost me nothing, as I would have paid the $10,000 to the government in taxes had I not donated it to charity. Thus, a credit is the strongest of the various available tax incentives. Unfortunately, as the law stands today, tax credits are not awarded for charitable gifts.

Under our current system, charitable gifts, within certain limits, are instead allowed as “deductions” from income before the tax rate is applied. In the example above, I would report $100,000 in gross income and take a charitable deduction of $10,000, leaving a taxable income of $90,000. I would then owe only $22,500 in taxes instead of $25,000. The deduction would result in tax savings of $2,500 and reduce the cost of my gift to $7,500. The $7,500 is called the “cost” of the gift because I would have been able to spend, save, or give that amount to loved ones had I not made the charitable gift.

The formula to determine the after-tax cost of a charitable gift of cash is Gift – T(Gift) = Cost, where T is the tax rate. Because my tax rate is 25%, my cost is $.75 per dollar given. If my tax rate were 40%, my cost would be $.60 on the dollar. If my rate were 10%, my cost would be $.90. The higher the tax bracket, the lower the after-tax cost of the gift. The cost of making a gift is lower for persons in higher tax brackets only because they would owe more in tax if the dollars were not donated to charity.

Another way to look at it is that Congress is giving up more revenue when a wealthy person makes a gift than when a lower-income person gives to charity. Under the current system, however, in no event does a donor at any income level actually pay income tax on the deductible amount given to charity.

Some have argued that it is unfair that the government gives up more revenue when a wealthy person gives than when gifts are made by others. Others point out that it is not fair that wealthy persons should have a lower after-tax cost of giving than others. Those two concerns are at the root of the administration’s proposal to limit the tax benefits of higher-income taxpayers to only the tax savings they would enjoy if they were in a 28% tax bracket. That way the government gives up no more than 28% per dollar donated, regardless of the donor’s tax bracket. It also means that the cost per dollar donated by the wealthy would be no less than $.72 per dollar donated even if they were in a higher tax bracket—or does it?

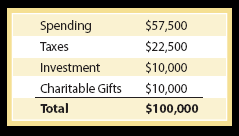

To get to the heart of the issue, it is important to return to the perspective of a donor considering making a gift. Let’s take the case of Ms. Greene. After looking at her overall finances, she decides to make a cash gift of $10,000 to her favorite charity. Regardless of her tax bracket, she must allocate $10,000 in cash to fund the gift.

Recall Ms. Greene has an income of $100,000. If she decides to give $10,000 to charity, invest $10,000 in mutual funds, pay taxes on the amount not donated to charity, and spend what remains, here is what her “budget” would look like:

Under current law, no tax is due on the amount given to charity, which is the case under current tax law. Now suppose Ms. Greene sees her tax rate increase on all of the income she did not give to charity. Her tax bill would then go up even if the amount donated remained the same. When taxes increase, then her spending, savings, or giving must decrease to keep the total outlays within $100,000.

But suppose instead of raising taxes on all income, Congress decides to impose a targeted tax increase. Imagine Congress accomplishes this by limiting the amount of revenue it is willing to forego on amounts donated by the wealthy. In effect, this is what the administration’s budget proposal would do.

How does it work?

Despite reports to the contrary in the media, no one is proposing limiting the amount that can be deducted for charitable gifts. The press in some cases has inaccurately reported that Congress would limit the amount that is deductible from 35% to 28%. That is not the case. Under the proposed legislation, a donor would still deduct the same amount as before, subject to normal adjusted gross income (AGI) limitations. What is limited is the amount of revenue Congress would give up as a result of the gift.

For example, suppose a taxpayer in the 35% tax bracket reports $100,000 in income taxed at that rate and donates $10,000 to charity. Under current law, this donor would deduct $10,000, reduce his taxable income by that amount, and lower his taxes by $3,500. If the maximum tax bracket were reduced to 28%, he would still deduct $10,000 but save only $2,800 in taxes.

Under the proposed changes, even though the donor is in the 35% tax bracket, Congress would pretend his maximum tax bracket is 28% when he takes his charitable deduction. The donor would then be able to reduce his taxes by only $2,800, not $3,500—a difference of $700.

This donor would still owe $700 in taxes. Therefore, he may give $10,000, take a tax deduction of $10,000, and still owe an additional $700 when the final bill is computed.

This proposal does more than simply raise or lower tax rates in general. For the first time, the federal government is considering taxing income that is given to charity.

Possible implications

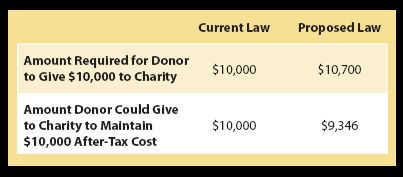

Let’s return to our donor above. If he had budgeted $10,000 to make charitable gifts, he would now have to budget $10,700 to make a $10,000 gift.

The additional $700 to be paid in taxes means he will have less to spend, invest, or give to loved ones. The only other alternative to keep his budget in balance is to reduce the gift amount from $10,000 to $9,346. He would retain the $654 difference to cover the additional tax due on the $9,346 he donated.

Any way you look at it, Congress is raising the cost of the gift in terms of cash outlay by approximately 7%.

If passed by Congress, the proposed changes would come into effect in 2011, the same year that, in another proposal, the maximum tax rate may be raised to 39%. The proposed tax increase would widen the “spread” between the maximum income tax rate (39%) and the rate at which charitable gifts may be deducted (28%) to 11%. A $10,000 gift would require $11,100 in income. If, given budget concerns, only $10,000 is available for the charitable gift, the actual gift to charity would need to be reduced to roughly $9,100, with the remaining amount paid in taxes. In this case the impact on larger campaign gifts could become more significant. Imagine how a donor would feel if faced with writing a check to the IRS for $111,000 to cover the tax on a $1 million fund-raising campaign contribution.

It is unclear how higher-income taxpayers will react to such changes, but it is certain that their accountants will see it as part of their professional role to explain this change and advise them how the “numbers” will work in their case.

Consider the similarities between this situation and the historical impact over the decades of the 50% of AGI limit. How many times have you heard a donor say, “I can’t give any more this year. My accountant tells me I have given all I can deduct.” Donors tend to cut their giving when told they owe tax on any amounts donated beyond the AGI limits.

In the case of this proposed change, however, higher-income donors and their accountants will not be able to avoid paying tax on amounts they donate to charity by monitoring their proximity to the 50% of AGI limit. Affected taxpayers will find that none of the dollars that are subject to the rule are deductible at full value.

The stated intent of the proposed tax law changes is to raise taxes on the wealthy. Whether that is advisable is beyond the scope of this article. This increase is slated to be accomplished, however, not through an across-the-board increase in tax rates on the wealthy but rather by imposing a targeted tax increase on amounts donated to charity by people with incomes over roughly $250,000. By that standard, this tax could impact a couple with mid-management jobs in high-cost areas of the country; it is certainly not a tax that will affect only the megarich.

No one can really predict the implications of this bill because there is no precedent for it. It would surely affect some charities more than others. Those with the strongest ties to donors would likely fare the best, with the impact felt most by charities to which donors may be giving solely out of social obligation or other less compelling motivations.

Again, our intention is simply to explain the structure and possible impact of the proposal, not to take a position on the advisability of this change. Regardless of what happens, charities will have to find a way to adjust to the resulting funding changes through budget reductions or other means.

If the issue is still in flux at the time you are reading this article, however, take a few minutes to reflect on what this proposal would really accomplish. Once you have decided how you feel about it, exercise your right to contact your representatives and make your opinion known.