by Robert Sharpe

Nonprofit managers have spent the last 20 years hearing about the “Great American Wealth Transfer,” which was predicted to usher in a Golden Age of Philanthropy with trillions upon trillions of dollars expected to flow to the U.S. philanthropic world.

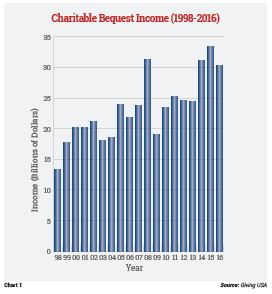

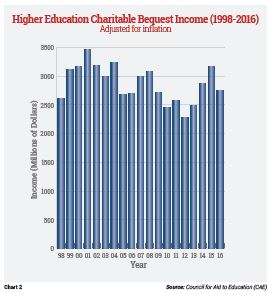

Unfortunately, for a number of reasons, this charitable windfall hasn’t yet materialized. In fact, according to industry reports from Giving USA and specialized reports from the Council for Aid to Education (CAE) detailing giving trends to higher education, when adjusted for inflation there’s been relatively little real increase in wealth transferred to charities through estates since 1998, when the transfer period was expected to begin (see Charts 1 and 2).

Over the last 18 years, bequests reported to charity totaled $428 billion,1 a fraction of the $1.7 trillion nonprofits were told to expect during that time frame.2 Keep in mind the period of the entire projected wealth transfer was 55 years, from 1998 to 2053. Simple math reveals that to hit the minimum projected charitable amount of $6 trillion for the entire transfer, bequest income to nonprofits will have to average $150 billion per year for the next 37 years, which is seven times the annual average seen over the past 18 years.

There have been adjustments to the original amount of the estimated wealth transfer over time, and one can quibble over the exact value of the assets to be transferred depending on various investment return assumptions. But, let’s put the ultimate dollar figure aside for now and focus more on what actually happened and what’s likely to transpire going forward.

Where’s the beef?

So, where exactly is the disconnect? What happened to stall the wealth transfer? Has it been permanently derailed or just delayed?

So, where exactly is the disconnect? What happened to stall the wealth transfer? Has it been permanently derailed or just delayed?

The answer may lie in a number of interrelated factors, including economic conditions, redistribution of wealth, demographic trends and other factors such as wealth “transferred” to the medical and health insurance sectors of the economy due to advances in medical care.

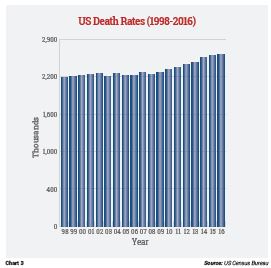

Keep in mind that the amount of wealth that’s transferred is a function not only of the amount of wealth overall and the number of recipients, but also of the trends in the number of individuals passing away. It’s interesting to note that from 1998 to 2010, the number of individuals passing away was less than projected by the U.S. Census Bureau; it was essentially flat and even down in some years for the first time in history (see Chart 3).

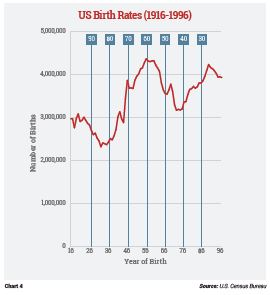

This was a result of two primary factors. First, the 20-year-long dip in birth rates in the United States between the mid-1920s to mid-1940s was predictably echoed by fewer deaths over the past 20 years (see Chart 4). As studies reveal that some 83 percent of bequest dollars come from those who die after the age of 80,3 this would naturally translate into fewer charitable decedents from roughly 2005 to 2025.

Adding to this demographic phenomenon has been the impact of advances in medical care that have resulted in extending life expectancies, leading to additional downward pressure on the number of charitable bequests.

The economy has also had an impact on the size of charitable bequests. When investment values plummeted at the outset of the Great Recession, many retirees “cashed out” of the markets and didn’t participate in the recovery.

There was, in effect, an unanticipated “wealth transfer” as subsequent record growth in investment values inordinately benefitted the relatively younger investors with higher risk tolerance who continued regular contributions to 401(k)s and other tax-favored retirement plans. This phenomenon resulted in wealth that was owned by older individuals prior to the crash essentially being transferred to a younger generation, while the older generation was still alive—rather than through estates at death.

Those who suffered recession-related losses have also struggled with meager returns on the assets that remained. Increasing numbers have, out of necessity, self-annuitized their assets, leaving less to distribute to both charitable and noncharitable beneficiaries at their deaths.

Darkest before the dawn?

Philanthropic planners should take heart, however, as the wealth transfer may now finally be beginning to accelerate. The number of deaths in the United States has risen again over the past few years, growing from the 2.4 to 2.5 million level from 2000 to 2010 to over 2.7 million decedents in recent years (see Chart 3).

Recent increases in death rates are being driven by the increase in births beginning in the mid-1930s as well as the “delayed” deaths of those in the G.I. Generation (those born between 1901 and 1924) and the Silent Generation (those born between 1925 and 1945), whose lives were extended by medical advances.

Beginning in the early years of the next decade, the mortality of the leading edge of the Baby Boomers should result in the commencement of the wealth transfer, albeit some 25 years after it was initially heralded.

Be prepared to aid the transfer

For many reasons, I believe it’s finally time to prepare for what truly may be a Golden Age of Philanthropy. Those who are ready to help donors execute their charitable plans can generate a substantial source of additional revenue for the charity they represent while helping donors make their gift of a lifetime. ■

This feature is based on an article directed to advisors in the September 2017 issue of “Trusts & Estates.” Click here to view the original article. Click here to read part two of this article featuring a look at what to expect from Baby Boomers.

This feature is based on an article directed to advisors in the September 2017 issue of “Trusts & Estates.” Click here to view the original article. Click here to read part two of this article featuring a look at what to expect from Baby Boomers.

Robert Sharpe is Chief Consultant and Chairman of Sharpe Group.

Endnotes

1. Giving USA 2016.

2. John J. Havens and Paul G. Schervish, “Millionaires and the Millennium: New Estimates of the Forthcoming Wealth Transfer and the Prospects for a Golden Age of Philanthropy,” Boston College Social Welfare Research Institute Report (Oct. 19, 1999).

3. Dr. Russell James, American Charitable Bequest Demographics (1992-2012) (2013), p. 54.