Earlier this year the Internal Revenue Service released in-depth information from federal estate tax returns for 2013 decedents that provides valuable clues about charitable bequest behaviors of wealthy Americans.

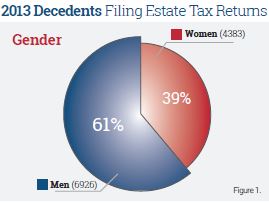

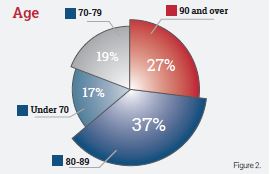

There were 11,309 estate tax returns filed for 2013 decedents, some 6,926 men and 4,383 women (see Figure 1). The vast majority of the decedents were older. Only 17 percent, or 1,909, were under the age of 70 when they died. The remaining 83 percent, or 9,400, were over the age of 70, and more estate tax returns were filed for decedents 90 and older than for all those who died under the age of 70 (see Figure 2).

Charitable estates

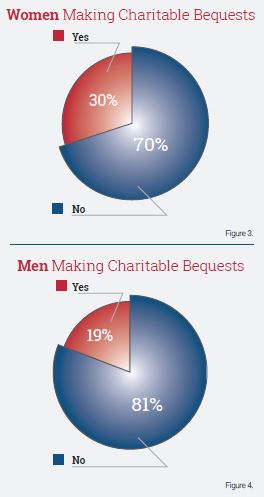

Nearly 25 percent of this group (some 2,634 decedents) provided for charitable bequests, and these bequests totaled $18.5 billion. This compares to estimates that five to six percent of the general population includes bequests. [American Charitable Bequest Demographics (1992-2012), Page 21, Russell James, J.D., Ph.D.] The wealthier charitable bequest population was nearly equally divided between men (1,333) and women (1,301). Based on the entire 2013 estate tax return population, it is clear that female decedents were significantly more likely to include a charitable bequest than their male counterparts. Some 30 percent of female decedents’ estate tax returns included a charitable provision; only about 20 percent of male decedents’ estate tax returns did so (see Figures 3 and 4). This finding is in line with results from previous studies.

Marital status

Whether one is married, widowed or single also plays an important role in the likelihood of including a charitable bequest. The majority of charitable bequests were made by decedents who were widowed, single, divorced or legally separated. This is no surprise since the primary beneficiary of most married people would be their surviving spouse. Still, there were major differences between male and female behaviors. Only 10 percent of married female decedents claimed a charitable deduction on their estate tax returns, while 40 percent of married male decedents included a charitable bequest. Overall, about 25 percent of charitable decedents were married and the balance were not. Charitable men were over four times more likely to be married than women.

Lessons learned

The charitable decedent population appears to be older than the general decedent population, and wealthy older men and women are more likely to include charitable bequests than the general population. The likelihood that an individual will make a charitable bequest, and the size of that bequest, increases with wealth. The most likely prospects are men and women who are not married.

The key to finding your organization listed among charitable beneficiaries is to identify and communicate with your donors with special attention to those who are wealthier and older. Sharpe Data Enhancement Services can help you analyze your constituent list and find those likeliest to make a bequest or other type of planned gift. Contact a Sharpe representative at info@SHARPEnet.com or 901.680.5300 or click here for more information. ■