Experienced development professionals will occasionally encounter wealthy donors whose first priority is not to make their children financially independent in their younger years. In many cases, such persons are entrepreneurs who have accumulated significant wealth during their lifetime. In fact, as many as 80% of millionaires have created their wealth from their own endeavors and have not experienced the benefit of an inheritance. Many successful people hope that their children will experience the same satisfaction of making their own way. These parents are concerned about their offspring and want to help them become financially responsible.

Given these facts, advisors often recommend a private foundation for the very wealthy, and, perhaps, an advised fund at a community foundation or elsewhere for those with lesser means. This strategy offers a way to shield assets from estate taxes while giving their adult children the opportunity to make charitable gifts to organizations and institutions of their choosing.

How one plan would work

On one occasion, I met with a couple in their mid-sixties who had amassed total wealth in the range of $20 million. They were understandably unhappy to learn that they could ultimately pay upwards of $9 million in estate taxes if they did not make plans to minimize or eliminate this tax. Given recent changes in Congressional leadership, some in this situation are less and less hopeful that the estate tax repeal scheduled for 2010 will ever take place. This couple had expressed a desire to “do something” for their two children (ages 32 and 34), but they didn’t want to give them “too much, too soon.”

One of their advisors recommended that they make gifts totaling $2 million to their children in a trust using their combined gift tax exemption amounts of $1 million each. They would then add amounts each year that they could give under their $12,000 per donee annual exclusion amounts. In 15 years, when the children reached ages 47 and 49, the balance remaining in the trusts would go to the children. With the balance, they were advised to leave what they could to their children free of tax at death and fund a private foundation with any remaining amount, thereby eliminating estate taxes that would otherwise be due. Their children would be named as trustees of the foundation and be given the right to make gifts to the charities they choose.

Neither parent was particularly happy with this plan because they felt they were substantially reducing their children’s inheritance in order to save taxes. Although this bothered them, they could see no other way out. Is there a better way?

An alternative plan

Suppose they were instead to create a charitable lead annuity trust today, funding it with $8 million? If the trust were established to pay 7.5%, or $600,000, to charities of the donors’ choosing each year for 15 years, the donors would enjoy a gift tax deduction of some $6.1 million, leaving a taxable gift of $1.9 million in the year the trust is created. Their gift tax exemption amounts could be used to offset this gift, resulting in a gift of $8 million (more or less, depending on the performance of the trust assets) to their children at a “cost” of their combined $2 million gift tax exemption amount. If they wished, the parents could direct that some portion of the lead trust payments be paid to charitable interests of their choosing and the balance to an advised fund at their local community foundation or elsewhere. If half of the payments were directed to an advised fund, the children could make suggestions for the distribution of some $300,000 per year.

The net result? The donors retain $12 million to use as they wish for the remainder of their lives, create an income stream of $9 million to charities of their choice, and provide an $8 million tax-free inheritance for their children in 15 years, the same point in time they initially wanted them to receive their inheritance. They have provided for their children as they wished in a way that fulfills their charitable intentions and eliminates the estate and gift tax on the $8 million gift to their children.

If they wish, the couple can continue their annual giving program to their children, and leave what they can to them free of tax from the remainder of their estate at death. With the balance of the assets, they might decide to fund a testamentary lead trust that will serve to fund various charities, a family foundation, an advised fund, or some combination thereof over time with the remainder distributed in the future to their children, grandchildren, or others. In that event, they will have totally eliminated tax on an estate of $20 million or more. The parents have thus “temporarily disinherited” their children through the creation of a “temporary foundation.” They can inform the children of the coming inheritance while letting them know they are “on their own” for the next 15 years.

A boom in lead trusts?

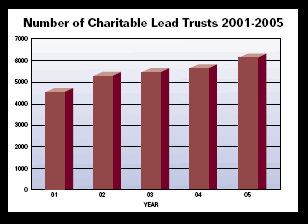

Reports from the IRS indicate that the number of charitable lead trusts has grown dramatically in recent years. In fact, while the number of charitable remainder unitrusts in existence has grown just one-half of one percent since 2001, the number of charitable lead trusts has grown by some 35%.

As of the end of 2005 there were 6,148 lead trusts in existence. The assets held in these trusts totaled approximately $15.1 billion. What may come as a surprise to some is the fact that 4,140, or 67%, of the trusts held assets of less than $1 million. These trusts held an average of $367,000. Overall, the average size of charitable lead trusts was $2.5 million. This indicates that more and more donors of relatively modest means are finding that charitable lead trusts can be an important part of their charitable and estate plans.

We believe that the future may hold even greater growth for charitable lead trusts. As the estate tax will have less of an impact at the death of many persons, an increasing number will be looking to minimize the impact of gift taxes on gifts to children and others while also fulfilling charitable gift commitments during their lifetime. Organizations that are prepared to structure major current and deferred gifts in this way will benefit through the creation of “temporary endowments,” in some cases in the form of charitable lead trusts. This is only one example of how understanding the interrelationship between donors’ philanthropic and other motivations can lead to significant gifts that might not otherwise be possible.

Editor’s note: This information is excerpted from the Sharpe seminar “Integrating Major and Planned Gifts.” See page 3 for more information about this professional development opportunity.